- Anonymouskeyboard_arrow_down

Summary:

The HELOC vs Refinance Calculator helps you decide the cheapest way to access equity in your home.

It compares a Home Equity Line of Credit (HELOC) which is interest-only and keeps your existing mortgage against a full refinance that wraps the borrowed amount into a new single mortgage.

The comparison uses net cost: interest paid minus principal repaid, so the refinance option is not unfairly penalised for paying down debt.

Note: Mobile browsers have a simplified UI which may not contain all controls. For best experience, a desktop browser is recommended.

How to open the calculator:

- Navigate to the Calculators page using the main menu.

- Find HELOC vs Refinance in the list and click the calculator icon.

[Screenshot: Calculators page showing the list of available calculators]

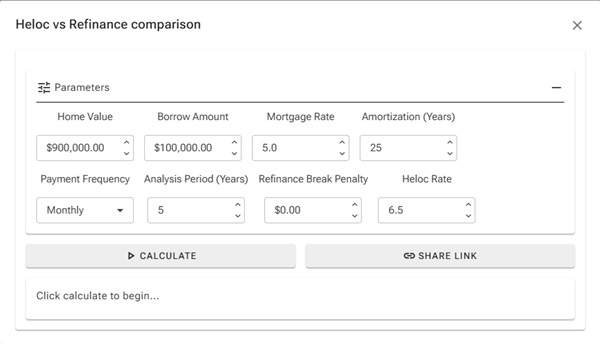

Input Parameters:

| Parameter | Description |

|---|---|

| Home Value ($) | Current appraised value of your home. |

| Equity Amount ($) | The amount of equity you want to access. |

| Current Mortgage Rate (%) | Your existing mortgage's annual interest rate is also used as the refinance rate. |

| Amortization (Years) | Used for both the existing mortgage and the new refinanced mortgage. |

| Payment Frequency | How often mortgage payments are made. |

| HELOC Rate (%) | The annual interest rate on the HELOC (typically Prime + a spread). |

| Break Penalty ($) | Any penalty owed for breaking your existing mortgage (enter 0 if at renewal). |

| Analysis Years | The number of years over which to compare the cost of each option. |

Note: The calculator assumes no existing mortgage balance (i.e. you own the home outright or are accessing pure equity). Available HELOC equity is capped at 80% of home value.

[Screenshot: HELOC vs Refinance calculator with inputs filled in]

How the comparison works:

HELOC option:

- Interest-only payments on the borrowed amount at the HELOC rate.

- The principal is never repaid during the analysis window. It remains outstanding.

- Net cost = total interest paid (pure cost, no equity offset).

Refinance option:

- The borrowed amount is added to the existing mortgage balance and refinanced at the current rate.

- Payments amortize the full balance, so principal is repaid each period.

- Net cost = total interest paid ? principal repaid + break penalty.

- This is fair: principal repaid is equity returned to you, not a true cost.

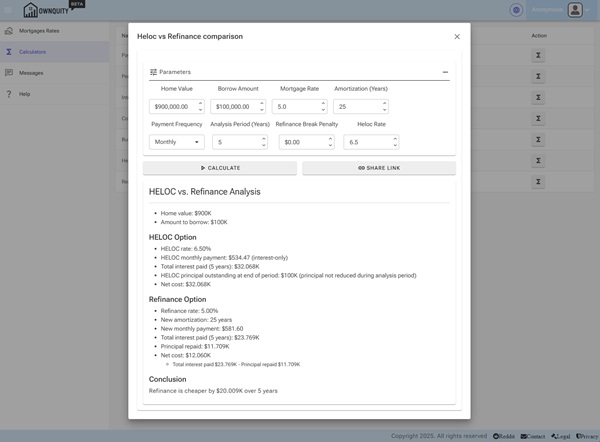

Reading the Results:

The HELOC Option section shows:

- HELOC monthly payment (interest only)

- Total interest paid over the analysis period

- Principal outstanding at the end (full borrowed amount is never reduced)

- Net cost

The Refinance Option section shows:

- New monthly payment

- Total interest paid over the analysis period

- Principal repaid over the analysis period

- Break penalty (if any)

- Net cost (interest ? principal repaid + penalty)

- Formula note showing the net cost calculation

The Conclusion states which option costs less and by how much.

[Screenshot: HELOC vs Refinance results showing both options and the conclusion]

Tips:

- HELOCs have lower initial payments but leave the full principal outstanding. a refinance pays down the loan and builds equity.

- If you plan to repay the borrowed amount within 2-3 years, the HELOC's lower total interest often wins.

- For longer time horizons the refinance typically wins due to the principal repayment credit.

- A large break penalty significantly narrows or eliminates the refinance advantage. enter the accurate penalty for a realistic comparison.

Additional Information:

- See the Penalty Calculator help article to estimate your break penalty before entering it here.

- See the Debt Consolidation Calculator help article if you plan to use the equity to pay off other debts.