- Anonymouskeyboard_arrow_down

Summary:

The Debt Consolidation Calculator compares the cost of keeping your existing debts (credit cards, lines of credit, car loans, etc.) against rolling them all into a single mortgage at a lower interest rate.

It helps you decide whether consolidating saves money in interest and simplifies your monthly cash flow.

Note: Mobile browsers have a simplified UI which may not contain all controls. For best experience, a desktop browser is recommended.

How to open the calculator:

- Navigate to the Calculators page using the main menu.

- Find Consolidate Debt in the list and click the calculator icon.

[Screenshot: Calculators page showing the list of available calculators]

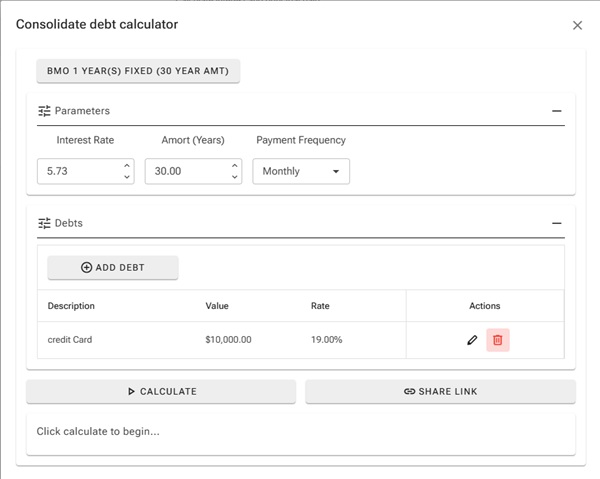

Step 1: Enter the consolidated mortgage terms:

| Parameter | Description |

|---|---|

| Interest Rate (%) | The mortgage rate you would consolidate into. |

| Amortization (Years) | The amortization for the consolidated mortgage. |

| Payment Frequency | How often the consolidated mortgage payments would be made. |

Step 2: Add your existing debts:

Click Add Debt to add each debt you want to consolidate.

[Screenshot: Debt consolidation calculator showing the Add Debt button and debt list]

[Screenshot: Debt consolidation calculator showing the Add Debt button and debt list]

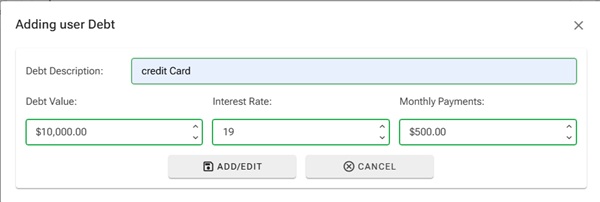

For each debt, enter:

| Field | Description |

|---|---|

| Description | A label to identify the debt (e.g. "Visa Card"). |

| Balance ($) | The current outstanding balance. |

| Interest Rate (%) | The current annual interest rate on the debt. |

| Monthly Payment ($) | Your current minimum or actual monthly payment. |

[Screenshot: Debt entry dialog with fields filled in]

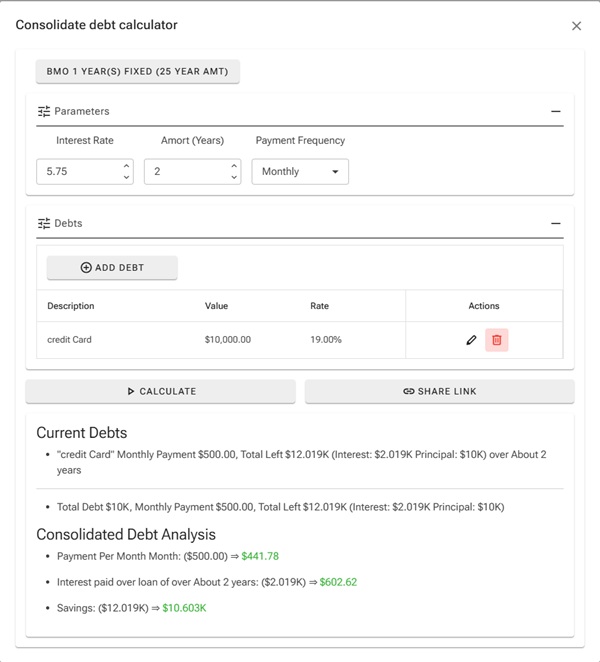

Reading the Results:

The results compare:

- Current debts total: sum of all outstanding balances, total interest paid at existing rates over the remaining terms.

- Consolidated mortgage: the new single payment, total interest paid at the mortgage rate over the amortization.

- Net savings: the difference in total interest between keeping debts vs. consolidating.

[Screenshot: Debt consolidation results showing savings breakdown]

Tips:

- Consolidating into a mortgage almost always reduces the interest rate, but extending the repayment period can offset savings. Use the shortest amortization you can afford.

- High-interest debts (credit cards at 20%+) benefit the most from consolidation.

- Consider whether your mortgage allows refinancing without a penalty before consolidating.

Additional Information:

- See the Penalty Calculator help article to estimate break costs if refinancing is required.

- See the HELOC vs Refinance Calculator help article to decide whether a HELOC or full refinance is best for accessing equity to consolidate.